Dwelling into Multiples - Decoding the science behind Pricing Multiples.

Why "expensive" stocks are often bargains, and "cheap" ones are often traps

In the world of investing, pricing multiples such as P/E (Price-to-Earnings) or EV/EBITDA are the most common languages spoken. But here’s the paradox that trips up most beginners: why does a slow-growing company trade at a massive 50x multiple, while a hyper-growth firm struggles at 15x?

What are Pricing Multiples (Price/Earnings or EV/EBITDA)

Most investors see a P/E ratio as the price we pay today for a unit of current earnings. That’s a static, backwards-looking view

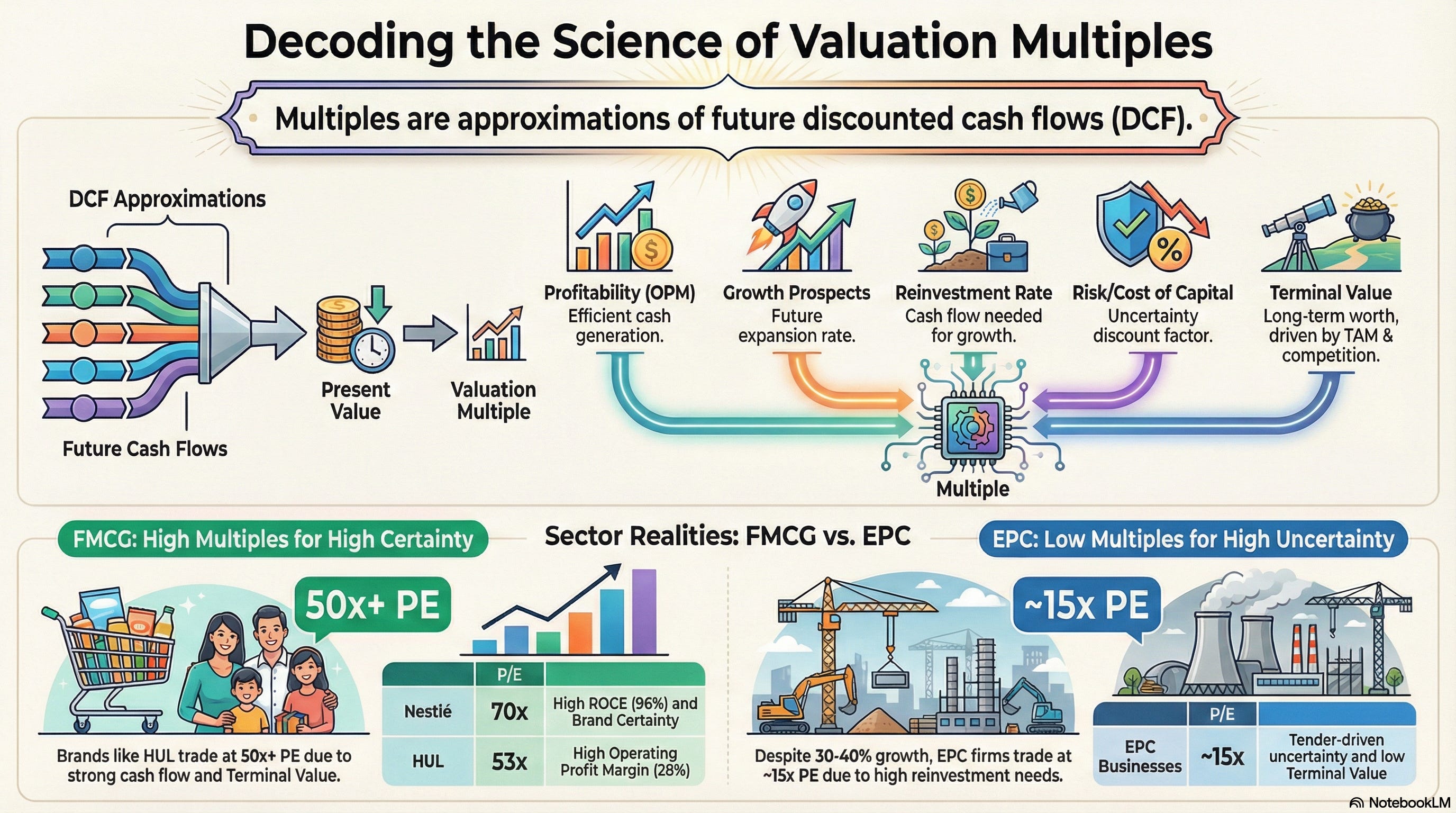

The key insight most people miss is that PE ratios aren't just about current earnings. They are actually sophisticated, shorthand approximations of Future Discounted Cash Flows (DCF). When you pay for a multiple, you aren't just buying today’s profit; you are bidding on the present value of every dollar that the company will ever make

The Theory of Value

In theory, the value of any asset—be it a stock, a bond, or a building—is the present value of all cash flows expected over its lifetime, discounted to today’s value based on the risk involved.

The problem? Projecting cash flows for the next 20 years is incredibly complex and prone to error. Because of this "math fatigue," we resort to trading multiples of similar companies as a shortcut.

Why reinvent the wheel when the market has already done the heavy lifting for similar companies?

What are the Cashflows or Free CashFlows

Imagine yourself as a business operator, operating a local kirana shop/grocery shop

The Money that you can take home will be determined by your operating profit margin, which is a factor of your gross margin/contribution margin per unit of sale x no of times you turn your inventory.

No of times you turn/sell your inventory and how quickly you get your money (debtor days) & the credit you get for the inventory purchase, determine your working capital needed - lower working capital means a lower reinvestment in inventory to fuel your business growth.

The Money that you can take home will be determined by your operating profit margin, any interest or debt payments to be made, and any money that needs to be reserved for buying additional inventory or capex for funding growth & whatever is left post that is the Free cash flow

So higher the Free cash flows, the higher the valuations should be & the higher the pricing multiples (PE or EV/EBITDA), given everything else is the same.

What Truly Drives the Multiple?

If you want to know why a stock trades where it does, look at these five drivers:

Profitability/OPM: Higher margins usually lead to higher multiples.

Growth Prospects: How fast the “pie” is expanding.

Reinvestment Rate: Companies that need less capital to grow (low working capital and high asset turnover) are rewarded with higher multiples.

Risk/Discount Rate: The cost of capital - smaller size companies are riskier, hence everything else same should get a lesser multiple.

Terminal Value: This is the “Heavy Hitter.” It’s driven by the Total Addressable Market (TAM) and the company’s “moat” or ability to capture it over decades.

This is why companies with high Return on Equity (ROE) or Return on Capital Employed (ROCE) trade with structurally large TAM trades at a premium.

Breaking Down FMCG's Pricing Multiples

Current multiples:

HUL: 53x PE, 28% OPM, 28% ROCE

Colgate: 47x PE, 35% OPM, 105% ROCE

Nestlé: 70x PE, 25% OPM, 96% ROCE

Despite a 6-7% historical annual growth rate, why do they trade at such high multiples?High Cash flow is generated per rupee of sale, driven by high OPM (25%)+, negative or low working capital days (less than 30), and high asset turnover (5x)

Massive Terminal Value -The market has strong certainty that they will capture the massive TAM (India’s FMCG use spend/capital is still low compared to the global average), primarily due to the established distribution points & brand value.

While EPC biz, which might be growing at 30-40% y/y, trades at 15xPE due to high w.c investment & low terminal value (EPC biz is tender or bid-driven biz, and high uncertainity that the company may not grow post a certain scale, hence a very low terminal value & a myopic view on the valuation - immediate 1-2 years + cyclicality in business.

Final Takeaways

Pricing multiples are not just random numbers; they are sophisticated signals about:

Future Free Cash generation ability.

Growth Trajectory and Terminal Value.

The “Story” behind the Moat.

The Golden Rule: Never invest based on a P/E ratio alone. Instead, use this framework to understand the reason behind the price

In case you liked my view, do subscribeto my page, till the time I find and share more mental frameworks on business analysis & investing.

I write such detailed valuation insights & company valuations on X. Do check it out, Twitter/X Profile